Cost Basis: Your Complete Personal Finance Guide

Understanding cost basis is not just for seasoned investors; it's a fundamental concept for anyone who buys, sells, or inherits assets. Without a firm grasp of your cost basis, you could pay more in taxes than legally required, struggle to make informed investment decisions, or even face penalties from the IRS. Many individuals, especially those new to investing or managing inherited property, overlook this crucial detail until tax season arrives, often leading to confusion and missed opportunities for tax savings. This comprehensive guide will demystify cost basis, explaining what it is, why it matters, and how to accurately calculate and track it for various types of investments. By the end of this article, you will have the knowledge to confidently manage your investments and optimize your tax obligations.

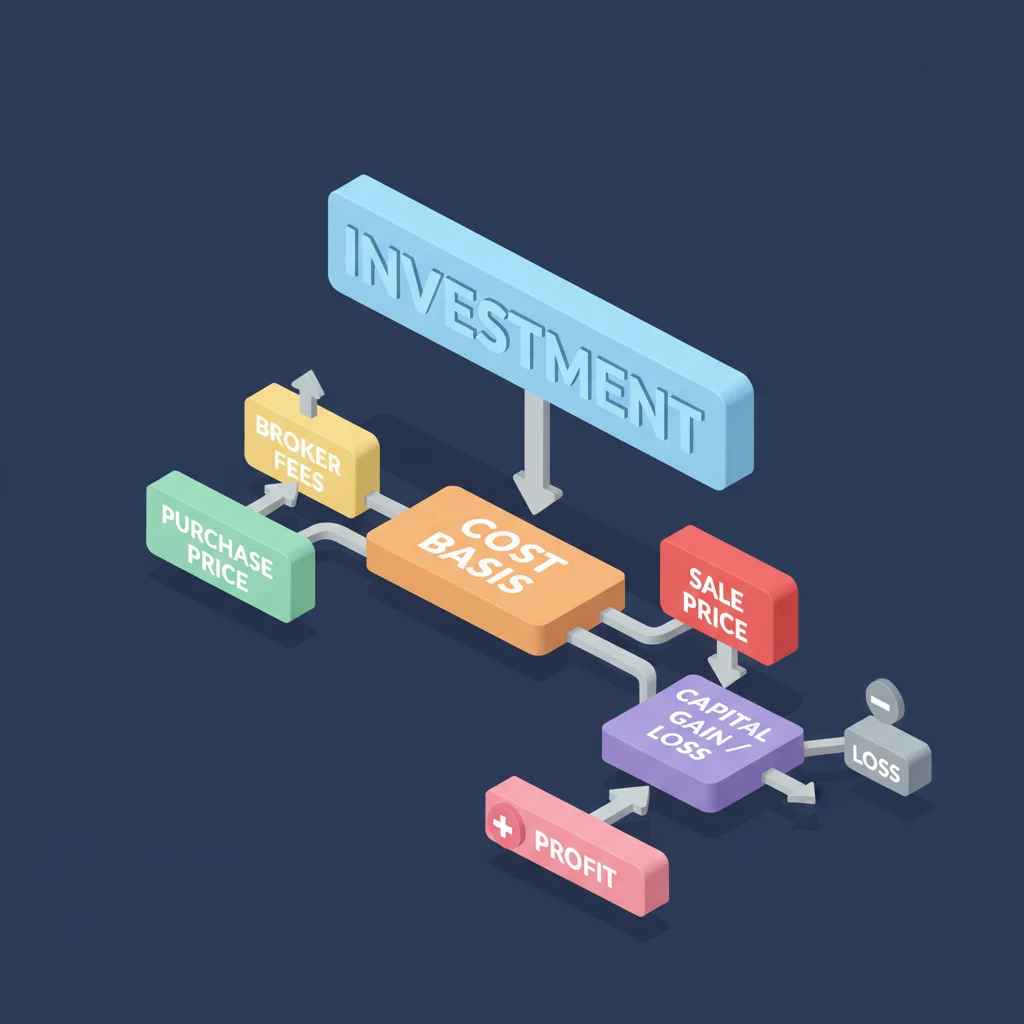

Cost Basis Definition: Cost basis is the original value of an asset, adjusted for various factors like commissions, fees, stock splits, and dividends, used to determine a capital gain or loss when the asset is sold.

What is Cost Basis and Why Does It Matter?

Cost basis is essentially your investment's starting point for tax purposes. It represents the total amount you've paid for an asset, including the purchase price and any associated costs like commissions or fees. When you sell an asset, the difference between the selling price and its adjusted cost basis determines your capital gain or capital loss. This gain or loss is then used to calculate the taxes you owe. Without accurately tracking your cost basis, you risk overpaying taxes on your investment gains or failing to claim valuable tax deductions for losses.

The Core Concept of Cost Basis

At its simplest, cost basis is the amount of money you've invested in an asset. This includes the initial purchase price. However, it's more nuanced than just the sticker price. It also incorporates other expenses directly related to acquiring the asset. For example, if you buy shares of a stock, the cost basis isn't just the price per share; it also includes any brokerage commissions you paid to execute the trade. Similarly, for real estate, the cost basis includes the purchase price, closing costs, and any significant improvements made to the property.

The primary reason cost basis matters is its direct impact on your tax liability. When you sell an investment for more than its adjusted cost basis, you realize a capital gain. This gain is subject to capital gains tax. Conversely, if you sell an investment for less than its adjusted cost basis, you incur a capital loss. Capital losses can be used to offset capital gains and, in some cases, a limited amount of ordinary income, reducing your overall tax burden. The IRS requires you to report your cost basis when you sell an investment, making accurate record-keeping essential.

Capital Gains and Losses Explained

Understanding the difference between capital gains and losses is crucial for tax planning. A capital gain occurs when you sell an asset for more than its adjusted cost basis. For example, if you buy a stock for $100 (your cost basis) and sell it for $150, you have a capital gain of $50. Conversely, a capital loss occurs when you sell an asset for less than its adjusted cost basis. If you buy a stock for $100 and sell it for $80, you have a capital loss of $20.

Capital gains are categorized into two types: short-term and long-term. Short-term capital gains are realized on assets held for one year or less. These gains are taxed at your ordinary income tax rate, which can be as high as 37% for the highest earners in 2026. Long-term capital gains are realized on assets held for more than one year. These gains are typically taxed at preferential rates: 0%, 15%, or 20%, depending on your taxable income. For 2026, for single filers, the 0% rate applies to taxable income up to $51,700, the 15% rate up to $577,600, and the 20% rate for income above that. Married couples filing jointly have higher thresholds. This distinction highlights the importance of holding investments for longer periods to benefit from lower tax rates.

Capital losses can be used to offset capital gains dollar-for-dollar. If your capital losses exceed your capital gains, you can deduct up to $3,000 of the remaining loss against your ordinary income each year. Any unused capital loss can be carried forward indefinitely to offset future capital gains or ordinary income. This strategy, known as tax-loss harvesting, is a powerful tool for reducing your tax bill.

Why Accurate Tracking Prevents Tax Headaches

Accurate tracking of your cost basis is not just good practice; it's a legal requirement and a significant tax advantage. The IRS mandates that you report your cost basis when you sell an investment. Brokerages typically report this information to the IRS on Form 1099-B, "Proceeds From Broker and Barter Exchange Transactions." However, the brokerage's reported cost basis might not always be accurate or reflect all adjustments, especially for older investments or those transferred between accounts.

If you don't have accurate records, you might end up using a default method (like First-In, First-Out, or FIFO) that results in a higher capital gain than necessary. For instance, if you bought shares at different prices over time, using a specific identification method could allow you to sell the shares with the highest cost basis, thereby minimizing your capital gain. Without proper documentation, you might not be able to prove your desired cost basis to the IRS, leading to potential audits, penalties, or simply overpaying taxes. According to IRS data from 2024, discrepancies in reported cost basis are a common trigger for inquiries, emphasizing the need for meticulous record-keeping.

Calculating Cost Basis for Different Assets

The method for calculating cost basis can vary depending on the type of asset you own. While the general principle remains the same – purchase price plus acquisition costs – specific adjustments and rules apply to stocks, mutual funds, real estate, and inherited assets. Understanding these nuances is key to accurate reporting.

Stocks and Exchange-Traded Funds (ETFs)

For stocks and ETFs, calculating cost basis typically involves the purchase price per share multiplied by the number of shares, plus any commissions or fees paid. However, several events can adjust this initial basis.

- Commissions and Fees: These are added to your cost basis. For example, if you buy 100 shares of a stock at $50 per share and pay a $7 commission, your total cost basis is ($50 * 100) + $7 = $5,007. Your cost basis per share is $50.07.

- Stock Splits: A stock split increases the number of shares you own while decreasing the price per share proportionally. Your total cost basis remains the same, but it's spread across more shares. If you owned 100 shares at a $50 cost basis ($5,000 total) and the stock splits 2-for-1, you now own 200 shares with a cost basis of $25 per share ($5,000 total).

- Reverse Stock Splits: The opposite of a stock split, this decreases the number of shares and increases the price per share. Again, your total cost basis remains unchanged.

- Dividend Reinvestment Plans (DRIPs): If you reinvest dividends to buy more shares, each new purchase has its own cost basis. This can complicate tracking, as you'll have multiple purchase lots at different prices.

- Return of Capital Distributions: These distributions reduce your cost basis. They are not considered taxable income until your basis reaches zero. After that, any further distributions are treated as capital gains.

When selling stocks or ETFs, you have several methods for determining which shares are sold, which directly impacts your capital gain or loss:

- First-In, First-Out (FIFO): This is the default method if you don't specify otherwise. It assumes you sell the oldest shares first. This can be disadvantageous if those shares have the lowest cost basis, leading to higher capital gains.

- Specific Identification (Spec ID): This is often the most tax-efficient method. It allows you to choose exactly which shares you are selling. You can select shares with a high cost basis to minimize gains or shares with a low cost basis if you want to realize a loss for tax-loss harvesting. Most brokerages allow you to specify this when placing a sell order.

- Average Cost: Primarily used for mutual funds, this method averages the cost of all shares purchased. While simpler, it's generally not allowed for individual stocks unless specific conditions are met.

Mutual Funds and REITs

Mutual funds and Real Estate Investment Trusts (REITs) have a slightly different approach to cost basis, particularly due to their frequent distributions and reinvestment options.

- Average Cost Method: For mutual funds, the IRS generally allows investors to use the average cost method. This simplifies tracking by averaging the purchase price of all shares you own. When you sell shares, the average cost per share is used to calculate your gain or loss. This method can be elected for all shares of a particular fund. Once elected, you generally cannot change it without IRS permission.

- Specific Identification: While less common for mutual funds, you can still use specific identification if you keep meticulous records of each purchase lot. This might be beneficial if you have significant price fluctuations and want to manage your gains or losses precisely.

- Reinvested Dividends and Capital Gains: Like DRIPs for stocks, reinvested dividends and capital gains distributions from mutual funds increase your total number of shares. Each reinvestment creates a new "lot" with its own cost basis. These reinvestments are taxable in the year they occur, even if you don't receive cash. Therefore, they also increase your cost basis, preventing you from being taxed on the same income twice when you eventually sell.

Example: Mutual Fund Cost Basis

| Date | Action | Shares | Price/Share | Commission | Total Cost |

|---|---|---|---|---|---|

| 01/15/2020 | Buy | 100 | $10.00 | $0 | $1,000 |

| 07/20/2021 | Reinvest Dividend | 10 | $12.00 | $0 | $120 |

| 03/10/2023 | Buy | 50 | $15.00 | $0 | $750 |

Total Shares: 160 Total Cost: $1,870 Average Cost Per Share: $1,870 / 160 = $11.69

If you sell 50 shares, your cost basis using the average cost method would be 50 * $11.69 = $584.50.

Real Estate

Real estate cost basis is often more complex due to the significant number of associated costs and potential adjustments over time.

- Initial Purchase Price: This is the starting point.

- Acquisition Costs: These are added to your basis. They include:

- Legal fees (attorney fees, title search)

- Survey fees

- Transfer taxes

- Recording fees

- Brokerage commissions (if paid by the buyer)

- Title insurance

- Capital Improvements: Money spent on improving the property, rather than just maintaining it, increases your cost basis. Examples include adding a new roof, renovating a kitchen, adding a room, or upgrading plumbing or electrical systems. These improvements must add value, prolong the useful life, or adapt the property to new uses. Regular repairs (e.g., fixing a leaky faucet, painting a room) are generally not added to the basis but are expensed in the year they occur.

- Depreciation (for rental properties): If the property is a rental or used for business, you must subtract depreciation claimed over the years from your cost basis. This reduces your basis, potentially increasing your capital gain when you sell. Depreciation recapture rules apply, meaning a portion of the gain attributable to depreciation may be taxed at ordinary income rates up to 25%, even if the overall gain is long-term.

- Casualty Losses: If you claim a casualty loss for damage to your property (e.g., from a fire or flood), your cost basis is reduced by the amount of the loss you deducted.

Example: Real Estate Cost Basis

| Item | Amount |

|---|---|

| Purchase Price (Home) | $300,000 |

| Closing Costs (title, legal, etc.) | $10,000 |

| New Roof (capital improvement) | $15,000 |

| Kitchen Renovation | $25,000 |

| Adjusted Cost Basis | $350,000 |

If you sell this home for $450,000, your capital gain would be $450,000 - $350,000 = $100,000.

Inherited Assets

Inherited assets receive a special tax treatment known as a step-up in basis. This means the cost basis of the asset is "stepped up" to its fair market value (FMV) on the date of the decedent's death. This can significantly reduce or even eliminate capital gains tax for heirs.

- Fair Market Value at Death: The cost basis for an inherited asset is generally its FMV on the date of the original owner's death. For example, if your parent bought stock for $10,000 and it was worth $100,000 when they passed away, your cost basis becomes $100,000. If you then sell it for $105,000, your capital gain is only $5,000, not $95,000.

- Alternate Valuation Date: The executor of the estate can elect to use an alternate valuation date, which is six months after the date of death, or the date the asset is sold or distributed if it occurs within those six months. This is typically done if the asset's value has decreased.

- Holding Period: Inherited assets are automatically considered to have a long-term holding period, regardless of how long the decedent or the heir actually owned them. This means any gains are taxed at the more favorable long-term capital gains rates.

- Community Property States: In community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin), both halves of community property receive a full step-up in basis upon the death of one spouse. In common law states, only the deceased spouse's half of jointly owned property receives a step-up. This distinction can have a significant impact on the surviving spouse's tax liability.

Example: Inherited Stock

| Scenario | Original Cost Basis | FMV at Death | Heir's Cost Basis | Sale Price | Heir's Capital Gain |

|---|---|---|---|---|---|

| Stock purchased by parent for $10,000 | $10,000 | $100,000 | $100,000 | $105,000 | $5,000 |

| Stock purchased by parent for $10,000 | $10,000 | $5,000 | $5,000 | $6,000 | $1,000 |

The step-up in basis is a major advantage for heirs and a critical component of estate planning.

Advanced Cost Basis Strategies and Considerations

Beyond the basics, several advanced strategies and considerations can further optimize your tax situation regarding cost basis. These include tax-loss harvesting, understanding wash sales, and the importance of accurate record-keeping.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy where you intentionally sell investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. This can significantly reduce your tax bill.

- Offsetting Gains: Capital losses can first be used to offset any capital gains you have realized during the year. If you have $10,000 in capital gains and harvest $7,000 in capital losses, your net capital gain is reduced to $3,000.

- Offsetting Ordinary Income: If your capital losses exceed your capital gains, you can deduct up to $3,000 of the net loss against your ordinary income (e.g., salary, interest income) each year. This $3,000 limit is for both single and married filing jointly taxpayers.

- Loss Carryover: Any capital losses exceeding the $3,000 limit can be carried forward indefinitely to future tax years. They retain their character as short-term or long-term losses and can be used to offset future capital gains or ordinary income. This makes tax-loss harvesting a powerful, long-term tax planning tool.

Example: Tax-Loss Harvesting

Suppose in 2026, you have:

- Long-term capital gain: $10,000

- Short-term capital gain: $5,000

- You decide to sell a stock at a long-term capital loss of $8,000 and a short-term capital loss of $4,000.

- Offsetting within categories:

- Net Long-Term Gain: $10,000 (gain) - $8,000 (loss) = $2,000

- Net Short-Term Gain: $5,000 (gain) - $4,000 (loss) = $1,000

- Total Net Capital Gain: $2,000 + $1,000 = $3,000. This $3,000 would be subject to long-term and short-term capital gains tax, respectively.

If, instead, you had:

- Long-term capital gain: $10,000

- Long-term capital loss: $15,000

- Net Long-Term Loss: $10,000 - $15,000 = -$5,000

- You have no other gains or losses.

- You can deduct $3,000 against ordinary income. The remaining $2,000 loss ($5,000 - $3,000) can be carried forward to 2027.

The Wash Sale Rule

The wash sale rule is an IRS regulation designed to prevent investors from claiming a tax loss while essentially maintaining their investment position. It states that if you sell an investment at a loss and then buy a "substantially identical" security within 30 days before or after the sale date (a 61-day window), the loss is disallowed for tax purposes.

- Substantially Identical: This means the same security or one that is very similar. For example, buying the same stock or an ETF that tracks the same index would likely be considered substantially identical. Buying a different stock in the same industry or an ETF that tracks a different index would generally not trigger the rule.

- Disallowed Loss: If a wash sale occurs, the disallowed loss is not lost forever. Instead, it is added to the cost basis of the newly purchased, substantially identical security. This effectively defers the loss until you sell the new shares.

- Impact on Holding Period: The holding period of the original shares is added to the holding period of the new shares. This can be beneficial if it helps the new shares qualify for long-term capital gains treatment sooner.

Example: Wash Sale

You buy 100 shares of XYZ stock for $100 per share. Later, you sell those 100 shares for $80 per share, realizing a $2,000 loss. Within 30 days, you buy 100 shares of XYZ stock again for $85 per share.

Because you repurchased XYZ stock within the 61-day wash sale window, your $2,000 loss is disallowed. Instead, your cost basis for the new 100 shares becomes $85 (purchase price) + $20 (disallowed loss per share, which is $2,000 / 100 shares) = $105 per share. This means your original $2,000 loss is now embedded in the higher cost basis of your new shares, and you will realize that loss when you eventually sell the new shares.

Gifts and Their Cost Basis

When you receive an asset as a gift, its cost basis is determined differently than inherited assets. There are two potential cost bases, depending on whether the asset is sold for a gain or a loss.

For a Gain: If you sell the gifted asset for a gain, your cost basis is generally the donor's original adjusted cost basis (the "carryover basis"). This means you inherit the donor's holding period as well.

For a Loss: If you sell the gifted asset for a loss, your cost basis is the lower of:

- The donor's adjusted cost basis, OR

- The fair market value of the asset at the time of the gift.

This "dual basis" rule prevents taxpayers from gifting assets with unrealized losses to another person solely to claim the loss. If the selling price is between the donor's basis and the FMV at the time of the gift, no gain or loss is recognized.

Example: Gifted Stock

| Scenario | Donor's Basis | FMV at Gift | Sale Price | Your Cost Basis (for gain) | Your Cost Basis (for loss) | Capital Gain/Loss |

|---|---|---|---|---|---|---|

| Donor bought for $100, gifted when worth $150, you sell for $180 | $100 | $150 | $180 | $100 | N/A | $80 gain |

| Donor bought for $100, gifted when worth $80, you sell for $70 | $100 | $80 | $70 | N/A | $80 | $10 loss |

| Donor bought for $100, gifted when worth $80, you sell for $90 (between) | $100 | $80 | $90 | N/A | N/A | No gain/loss |

The Importance of Record-Keeping

Meticulous record-keeping is paramount for accurate cost basis tracking. While brokerages provide Form 1099-B, it's not always exhaustive or perfectly accurate, especially for older investments, transfers, or complex situations like wash sales or inherited assets.

- What to Keep:

- Purchase Confirmations: These show the date, price, number of shares, and commissions.

- Dividend Reinvestment Statements: For DRIPs and mutual funds, these show new share purchases and their cost.

- Statements of Corporate Actions: Documents related to stock splits, mergers, or spin-offs.

- Gift Tax Returns (Form 709): If you received a gift, this can help establish the donor's basis or FMV at the time of the gift.

- Estate Documents: For inherited assets, the decedent's death certificate, appraisal documents, and estate tax returns (Form 706) are crucial for establishing the step-up in basis.

- Brokerage Statements: Monthly or annual statements provide a summary.

- Receipts for Home Improvements: For real estate, keep detailed records of all capital improvements.

- How Long to Keep Records: The IRS generally recommends keeping records for at least three years after the date you file your original return or two years from the date you paid the tax, whichever is later. However, for investment property, especially real estate, it's wise to keep records indefinitely or at least until seven years after you sell the asset and report the gain or loss. For assets like inherited property, records from decades ago might be needed.

- Digital vs. Physical: Store records securely, whether digitally (cloud storage, external hard drive) or physically (fireproof safe). Digital copies are often easier to organize and retrieve. Many financial advisors recommend using a combination of both.

Tools and Resources for Tracking Cost Basis

Managing your cost basis doesn't have to be a manual, overwhelming task. Several tools and resources are available to help you track your investments accurately and efficiently, from brokerage statements to specialized software.

Brokerage Statements and Tax Forms

Your brokerage firm is your primary source of cost basis information for most publicly traded securities.

- Form 1099-B: This form, issued annually by your brokerage, reports the proceeds from sales of stocks, bonds, and other securities. Crucially, it also reports the cost basis for "covered securities" (generally those acquired after January 1, 2011). For these, the brokerage is required to track and report the cost basis to both you and the IRS.

- Non-Covered Securities: For securities acquired before January 1, 2011, or in certain other situations, the brokerage may not report the cost basis to the IRS. In these cases, the 1099-B will indicate that the basis was "not reported to the IRS," and you are solely responsible for calculating and reporting it. This is where your personal records become vital.

- Monthly and Annual Statements: These statements provide detailed transaction histories, including purchase dates, prices, and any reinvested dividends. They are essential for verifying the information on your 1099-B and for tracking non-covered securities.

- Online Portals: Most brokerages offer robust online platforms where you can view your cost basis information, sometimes even allowing you to select different cost basis methods (like specific identification) before selling. Familiarize yourself with these features.

While brokerages provide a great starting point, always cross-reference their data with your own records, especially for complex transactions or older assets.

Personal Finance Software

For more comprehensive tracking, particularly if you have accounts across multiple brokerages or own diverse asset types, personal finance software can be invaluable.

- Quicken, Personal Capital (Empower), Fidelity Full View, Mint: These platforms allow you to link all your financial accounts – banking, investment, retirement, and even real estate. They can often import transaction data, categorize expenses, and track your investment performance. While they may not always calculate cost basis with the same precision as a dedicated tax software, they provide a centralized view of your holdings and can help you organize the data needed for tax preparation. Many offer tools to track capital gains and losses, and some even integrate with tax software.

- Spreadsheets (Excel, Google Sheets): For those who prefer a hands-on approach, a well-organized spreadsheet can be an effective way to track cost basis. You can create columns for purchase date, number of shares, price per share, commissions, total cost, and sale details. This method offers complete control and customization but requires diligent manual entry and updates. Templates are available online to help you get started.

Tax Software Integration

When tax season arrives, your cost basis data becomes critical. Tax preparation software is designed to handle this information efficiently.

- TurboTax, H&R Block Tax Software, TaxAct: These popular tax software programs allow you to import your 1099-B forms directly from many brokerages. They will then guide you through reporting your capital gains and losses on Schedule D (Capital Gains and Losses) and Form 8949 (Sales and Other Dispositions of Capital Assets).

- Manual Entry: If you have non-covered securities or need to make adjustments, these programs also allow for manual entry of cost basis information. This is where your meticulously kept personal records or spreadsheet data will be most useful.

- Guidance on Wash Sales and Other Rules: Tax software often includes built-in checks and guidance on complex rules like wash sales, helping you avoid common errors and ensure compliance with IRS regulations. This can be particularly helpful for investors who engage in frequent trading or tax-loss harvesting.

Financial advisors often recommend using a combination of these tools: leveraging brokerage statements for primary data, using personal finance software for overall portfolio tracking, and then utilizing tax software for final reporting. This multi-layered approach helps ensure accuracy and reduces the risk of errors.

Common Mistakes and How to Avoid Them

Even with the best intentions, investors can make mistakes when dealing with cost basis. These errors can lead to overpaying taxes, underreporting income, or facing penalties. Being aware of these pitfalls is the first step to avoiding them.

Ignoring Small Transactions and Fees

It's easy to overlook small details like trading commissions, transfer fees, or even tiny reinvested dividends. However, these seemingly minor amounts can add up and significantly impact your cost basis over time.

- Commissions and Fees: Always add these to your purchase price. A $7 commission on a $1,000 stock purchase increases your basis by 0.7%, which can matter when calculating gains or losses. Many brokerages now offer commission-free trading, but some still charge for certain asset types or services.

- Reinvested Dividends: When dividends are reinvested, they purchase additional shares. Each reinvestment creates a new cost basis for those new shares. Forgetting to add these to your overall basis means you'll be taxed on them again when you sell, essentially double taxation. This is a very common oversight for mutual fund investors.

- Transfer Fees: If you transfer assets between brokerages, there might be fees. While these might not always directly adjust the cost basis of the security itself, they are part of your overall investment cost.

Solution: Keep all transaction confirmations, even for small amounts. Regularly review your monthly and annual statements to ensure all activity is captured. Use software that automatically tracks these details where possible.

Mismanaging Wash Sales

The wash sale rule is one of the most frequently misunderstood and violated tax rules for investors. Failing to properly identify and adjust for wash sales can lead to disallowed losses and potential IRS scrutiny.

- Ignoring the 30-Day Window: Many investors forget the 30-day "before and after" rule, thinking it only applies to immediate repurchases.

- "Substantially Identical" Misinterpretation: Assuming that buying a different but similar ETF or stock avoids the rule can be a mistake. While a different company in the same sector is usually fine, an ETF tracking the exact same index as one you just sold at a loss might be problematic.

- Across Different Accounts: The wash sale rule applies across all your accounts, including IRAs and even accounts held by your spouse. Selling a stock at a loss in a taxable brokerage account and buying it back in your Roth IRA within 30 days still triggers a wash sale, and the loss is permanently disallowed (not added to the IRA basis).

Solution: Be acutely aware of the wash sale rule when considering selling an investment at a loss. If you plan to repurchase a similar security, wait at least 31 days. If a wash sale does occur, ensure your tax software or accountant correctly adjusts the basis of the new shares.

Neglecting Record-Keeping for Non-Covered Securities

As mentioned, brokerages are only required to track cost basis for "covered securities" (generally those acquired after 2011). Many long-term investors still hold "non-covered securities" purchased years ago.

- Lost Records: For older investments, original purchase confirmations or statements might be lost. This makes it challenging to prove your cost basis to the IRS.

- Default to Zero Basis: If you cannot provide a cost basis for a non-covered security, the IRS may assume your cost basis is zero. This means your entire sale proceeds would be treated as a capital gain, leading to a significantly higher tax bill.

- Transferred Assets: When assets are transferred between brokerages, especially older ones, the receiving brokerage may not receive or correctly track the original cost basis information.

Solution: Digitize all old investment records immediately. If records are truly lost, contact the original brokerage or transfer agent for historical statements. If all else fails, consult a tax professional to determine the best course of action, which might involve estimating basis based on historical market data (though this can be challenging to defend).

Not Understanding Inherited or Gifted Basis Rules

The rules for inherited and gifted assets are unique and often confused, leading to incorrect tax reporting.

- No Step-Up for Gifts: A common mistake is assuming gifted assets receive a step-up in basis like inherited ones. They do not; they carry over the donor's basis (or the lower of basis/FMV for losses).

- Incorrect FMV for Inherited Assets: Using an incorrect fair market value at the time of death for inherited assets can lead to miscalculations. This value should typically be determined by the estate's executor or an appraisal.

- Holding Period Confusion: Remember that inherited assets always get a long-term holding period, regardless of actual ownership duration. Gifted assets carry over the donor's holding period.

Solution: For inherited assets, obtain a copy of the decedent's death certificate and any estate valuation documents. For gifted assets, ask the donor for their original purchase records. If the donor is deceased, the executor of their estate should have this information. Always consult with an estate attorney or tax professional for clarity on these complex rules.

By being diligent in your record-keeping, understanding the specific rules for different asset types, and leveraging available tools, you can avoid these common cost basis mistakes and optimize your financial outcomes.

Frequently Asked Questions

What is the difference between cost basis and market value?

Cost basis is the original price you paid for an asset, adjusted for fees and other factors, used to calculate capital gains or losses for tax purposes. Market value is the current price at which an asset could be sold in the open market today.

Can I choose which shares to sell to optimize my cost basis?

Yes, for stocks and ETFs, you can typically use the specific identification method to choose which shares (or "lots") to sell. This allows you to select shares with a higher cost basis to minimize gains or shares with a loss to harvest for tax purposes.

What happens if I don't know my cost basis?

If you don't know your cost basis, especially for "non-covered securities" (generally acquired before 2011), the IRS may assume your cost basis is zero. This means your entire sale proceeds would be treated as a capital gain, leading to a much higher tax liability. You should try to reconstruct your basis using old statements or by contacting your brokerage.

Does cost basis apply to cryptocurrency?

Yes, cost basis applies to cryptocurrency. Each purchase of cryptocurrency creates a new cost basis. When you sell, trade, or otherwise dispose of crypto, you realize a capital gain or loss based on the difference between the selling price and your cost basis. The IRS treats cryptocurrency as property for tax purposes.

How do dividends affect my cost basis?

If you receive cash dividends, they don't directly affect your cost basis. However, if you participate in a dividend reinvestment plan (DRIP), the reinvested dividends purchase new shares. Each new purchase has its own cost basis, which increases your overall cost basis in the investment.

Is the cost basis the same for inherited property as for gifted property?

No, they are different. Inherited property receives a step-up in basis to its fair market value on the date of the decedent's death. Gifted property generally carries over the donor's original cost basis. This distinction is crucial for calculating capital gains.

How long should I keep records related to cost basis?

The IRS generally recommends keeping tax records for at least three years, but for investment property, especially real estate, it's wise to keep records indefinitely or at least seven years after you sell the asset. For inherited assets, records from the decedent's estate are crucial.

Key Takeaways

- Cost basis is fundamental for tax planning: It's the adjusted original value of an asset used to determine capital gains or losses, directly impacting your tax liability.

- Accurate tracking prevents overpayment: Without proper cost basis records, you risk paying more in taxes than legally required or missing out on valuable tax deductions from losses.

- Different assets have different rules: Stocks, mutual funds, real estate, and inherited assets each have specific methods and adjustments for calculating cost basis.

- Tax-loss harvesting is a powerful strategy: Intentionally selling assets at a loss can offset capital gains and up to $3,000 of ordinary income annually, with unused losses carried forward.

- Beware of the wash sale rule: Selling an investment at a loss and repurchasing a "substantially identical" one within 30 days before or after the sale will disallow the loss for tax purposes.

- Meticulous record-keeping is non-negotiable: Keep all purchase confirmations, statements, and relevant documents for years, ideally digitally and physically, to support your reported cost basis.

- Leverage available tools: Use brokerage statements, personal finance software, and tax preparation programs to help manage and report your cost basis accurately.

Conclusion

Understanding and accurately tracking your cost basis is a cornerstone of effective personal finance and investment management. It's not merely an accounting exercise but a critical component that directly influences your tax obligations and investment decisions. By mastering the concepts of initial basis, adjustments, and the various methods for different asset types, you empower yourself to minimize capital gains taxes, effectively utilize capital losses, and avoid potential IRS penalties. The effort you put into meticulous record-keeping and leveraging available tools will pay significant dividends, quite literally, in tax savings and financial peace of mind. Take control of your financial future by making cost basis a priority in your investment strategy.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or tax advice. Always consult a qualified financial advisor before making investment decisions.

The information provided in this article is for educational purposes only and does not constitute financial, investment, or legal advice. Always consult with a qualified financial advisor, tax professional, or legal counsel for personalized guidance tailored to your specific situation before making any financial decisions.

Comments

No comments yet. Be the first to comment!

More from Personal Finance

Explore Related Guides

Expert reviews of Gold IRA companies, rollover guides, fees, and IRS rules.

Comprehensive investment strategies covering stocks, bonds, ETFs, crypto, and real estate.

Compare banking products, interest rates, and strategies to maximize your savings.